Rosie O’Donnell says her grandparents’ Irish heritage qualifies her for citizenship application.

Day: October 7, 2025

Getty Images; Charly Triballeau/AFP via Getty Images; Alyssa Powell/BI

- David Ellison’s plans for his media empire are taking shape, bolstered by his father’s billions.

- Ellison’s moves show he’s willing to shake up legacy institutions and throw around cash.

- Employees at his company, Paramount, and other media insiders are feeling a mix of fear and excitement.

Big changes are happening in media — and one last name is at the center of it all: Ellison.

David Ellison is showing his ambitions are far greater than using media to buy more influence and Hollywood glamour. The son of tech billionaire Larry Ellison is shaking up storied institutions in news and entertainment as he seeks to build Paramount into a new media empire at lightning speed.

The clearest sign yet of Ellison’s willingness to ruffle feathers and fundamentally remake iconic American media brands was his Monday installation of Bari Weiss atop Paramount’s CBS News, the 98-year-old institution home to the likes of Walter Cronkite and “60 Minutes.”

Weiss, a former New York Times Opinion writer who resigned from The Gray Lady in 2020, has spent the years since building an anti-woke alternative to traditional media. That effort, The Free Press, is far from CBS News in sensibility and approach. It’s digital-first, subscription-focused, peppered with commentary, and routinely takes stances on hot-button issues, such as Israel’s war in Gaza and campus speech.

Daniel Paik

In buying The Free Press for about $150 million and putting Weiss in charge of CBS News as editor-in-chief, Ellison is sending a message: I’m not just a walking checkbook.

Warner Bros. Discovery, with its century-old studio and established news network CNN, could be his next target, according to a Wall Street Journal report from last month, which said the Ellison family was interested in acquiring it.

Ellison’s move fast and break things approach — backed by his father’s billions — has inspired both anticipation and fear among his employees and industry insiders. His bold plans to shake up some of entertainment’s most venerable brands could lead to a new industry powerhouse, but come with casualties.

“There’s a vision at the top — we didn’t have that,” a veteran Paramount software engineer said.

The Ellison media portfolio could soon influence everything from TikTok videos — Trump has said Larry Ellison will be a major player in TikTok’s US spin-off — to TV news and films on the silver screen. Further media consolidation could also result in thousands of layoffs and fewer studios available to fund TV and film projects.

“It’s an asteroid hitting Hollywood,” Adam Conover, a comedy writer who frequently speaks out on Hollywood labor issues, said of a potential merger of Paramount and WBD. “It’ll further hasten the end of the entertainment industry in LA.”

Hollywood’s hopes and fears

When whispers first began that Ellison was interested in buying Paramount in 2023, Hollywood seemed to breathe a collective sigh of relief.

Prior to Ellison, Paramount was floundering. There was a drawn-out sale process under Shari Redstone, internal conflict, and a failure to keep pace with the likes of Netflix and Disney in a rapidly changing industry.

Ellison, 42, brought Hollywood bona fides from his success with Skydance, with hits like “Top Gun: Maverick” and several “Mission: Impossible” installments.

Lia Toby/Getty Images for Paramount Pictures

He also brought cash. His father, the second-wealthiest person in the world, seemed willing to back his son’s ventures.

“You can’t underestimate the second richest person in the world,” a talent agent said as the deal closed in August. “I think we’re all optimistic.”

The younger Ellison quickly got to spending. He hired Cindy Holland, a prominent exec who helped make Netflix a streaming superpower, and vowed to roughly double Paramount’s film output. He shelled out over $7 billion to secure the US rights to UFC and poached top talent, including the Duffer brothers, who created “Stranger Things.”

“Everywhere you look, he’s throwing money,” LightShed Partners media analyst Rich Greenfield said. “That’s what Hollywood gets excited about.”

A bigger wave of disruption

As Ellison’s broader plans have begun to take shape, the optimism has taken on a jittery edge.

There’s a “nervous energy” at Paramount, an engineering manager said. Ellison is seeking to cut $2 billion in existing spending, and thousands of layoffs are anticipated.

“We’ve been bracing for impact for a year,” a Paramount marketing employee said of potential layoffs.

That could be just the opening act if the Ellisons actually buy WBD and merge the Hollywood giants. Forming a mega-studio would reorganize Hollywood as we know it, leading to further job cuts, one fewer buyer of content, and — if CBS and CNN were to combine — a larger potential kingdom for Weiss.

“On the surface, having a financially healthy and strong Paramount is great for Hollywood. The danger comes in if this is step one to multistudio consolidation,” Greenfield said.

Ellison has also shown an un-Hollywood-like embrace of technology. In a town that prides itself on its time-honored studio lots and has largely been cautious about artificial intelligence, Ellison talks about building a “studio in the sky” and harnessing AI to create content faster and on the cheap.

Then there’s the question of politics. While Larry Ellison has long been an outspoken Trump ally, David Ellison donated to Biden as recently as last year and has more opaque politics.

Anna Moneymaker/Getty Images

That hasn’t stopped the angst around David Ellison from taking on a political tone, and the appointment of Weiss — whose The Free Press is perceived in media circles as friendly to both conservatives and billionaires — isn’t helping.

“We Americans have to be concerned about the consolidation of huge billionaires getting control of nearly all the major news outlets,” former longtime CBS News anchor Dan Rather said on a radio show last month.

For those who worry about what Ellison’s vision will lead to, the question remains: Is there any sustainable alternative? A Hollywood ending may not be possible for the old Hollywood giants.

Streaming hasn’t made up for the decline of linear TV, while YouTube and social media are gobbling up more of people’s time.

Wall Street analysts pointed out that many of Ellison’s potential cuts would likely be in Paramount’s fading linear TV business, home to networks like Nickelodeon and Comedy Central. If it weren’t Ellison holding the hatchet, someone else would be. And a CBS viewed as “less left-leaning” may be good for the business under the Trump administration, analyst Ric Prentiss of Raymond James wrote.

Paramount could be a “dynamic global media company,” Band of America analyst Jessica Reif Ehrlich wrote when the merger closed. “However, there are no easy fixes.”

Read the original article on Business Insider

Moment police dog saves handler from shovel wielding arsonist as he attempted to burn down flat. The man attempted to hit PD Yoiko with a shovel and threatened any officers who came near him. PC Marsden managed to block this attempted hit on Yoiko and the man was subsequently arrested and sentenced to four years in prison.

Getty Images; Tyler Le/BI

A favorite adage of economists, market watchers, and financial journalists alike is that the American consumer is the engine of the US economy. If spending is not slowing, the thinking goes, the economy and labor market will be fine. It’s true that consumer spending represents a significant share of the economy, accounting for roughly two-thirds of the country’s GDP.

The truism is inspiring optimism about the economy’s current trajectory, given the recent strength of retail sales and other data on how people are spending their money. I think the causality here is backward. A consumer slowdown is never the precipitating cause of an economic slump. Usually, consumption falls after employment materially cracks. When Americans stop spending, by that time, it’s already too late.

While Americans continue to spend their way through their troubles, it may not prevent an economic slump from taking hold.

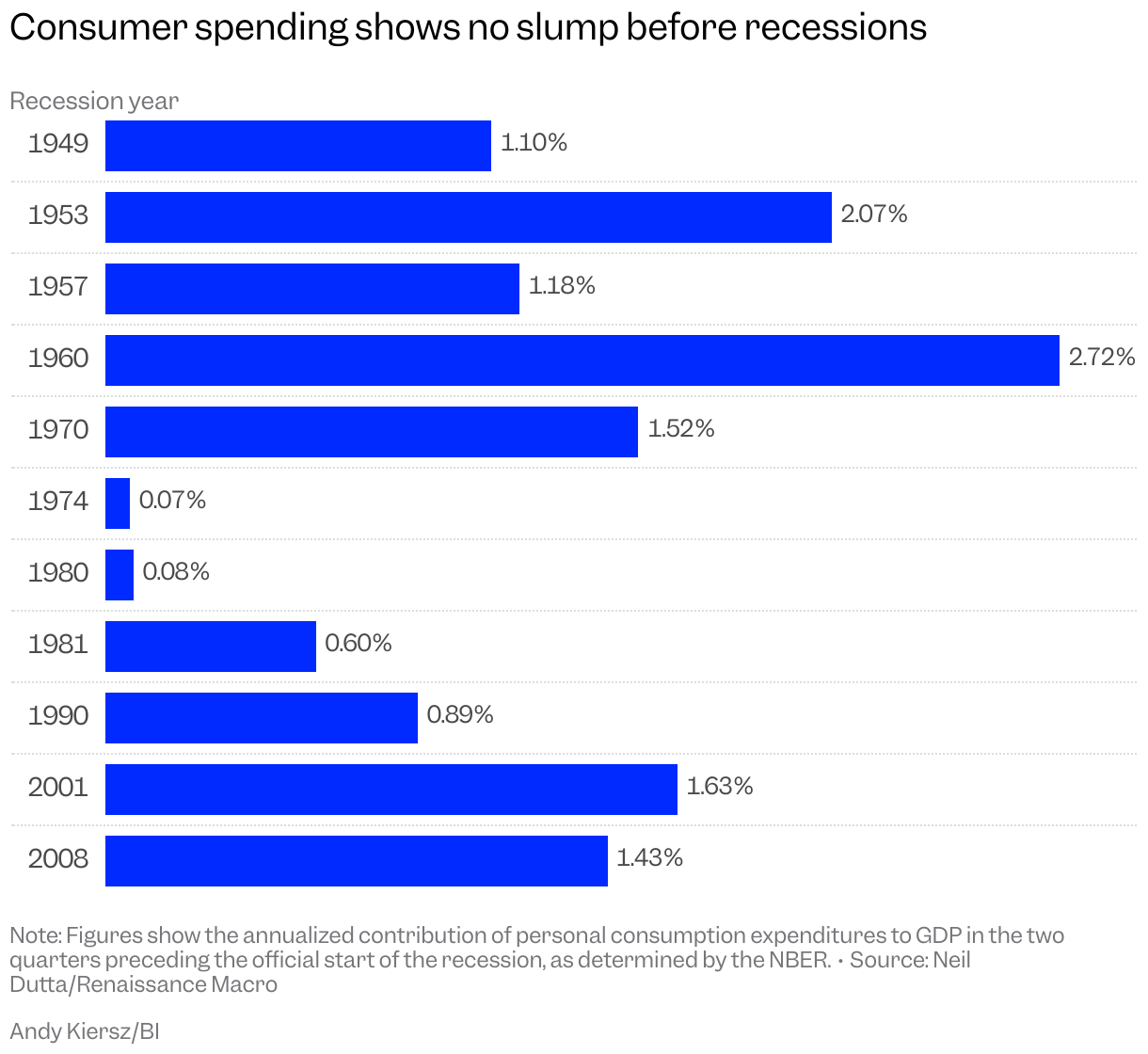

The notion that consumer spending can save the country from a recession contradicts several historical trends. For starters, consumption has managed to grow modestly in previous economic slumps. In several of the post-World War II recessions — 1948, 1970, 1982, and 2001 — real consumption expanded during the downturn. In other words, during those recessions, the best that spending could do was to help economic conditions from deteriorating further, cushioning the blow rather than preventing it altogether. In other periods of negative growth, consumption declined substantially, so that on average, its contribution to GDP during recessions is close to zero.

Next, consumption has never declined before an economic slump; it’s always happened after the economy began to go into the tank. Therefore, the growth in recent quarters does not look especially unusual. Assuming tracking estimates for the current quarter end up in the ballpark, average annualized growth in real consumer spending is expected to run at about 2.2% in the first two quarters of 2025. This is slightly slower than consumption growth in the two-quarter period preceding each of the last three recessions, but it’s hardly out of the ordinary.

Let’s deepen this analysis by breaking out the various types of major spending: durable goods, such as washing machines and TVs; nondurable goods like T-shirts and groceries; and services, encompassing everything from restaurants to movie tickets. Prior to previous recessions, the most common signal from these categories was Americans cutting back on big-ticket durables rather than cutting spending in service industries. As our figure shows, going back over the past 11 cycles, people decreased their expenditures on durable goods in the two quarters preceding the recession just over half the time. And during recessions, durable goods spending tends to fall while spending on services holds up. So far this year, spending on durables has been about flat. At the very least, this suggests a degree of caution among Americans when it comes to making big-ticket spending decisions that could portend more trouble coming down the line.

One confounding variable, of course, is the degree to which President Donald Trump’s herky-jerky tariff announcements are influencing the data, creating a push and pull in consumer behavior regarding durables. The threat of tariffs may have prompted people to pull forward activity, making big purchases before anticipated price hikes, while the hope for tariff removals might cause consumers to wait it out. On the other hand, the big story in the first half of this year has been the slowing of services spending, which is likely less sensitive to tariff news. This suggests that if you’re waiting for the consumer to make a call about a turn in the business cycle, you’re likely waiting too long. The recession red light is already lit by the time consumption contracts, and sometimes it does not fall at all.

America’s job market is looking weak

The better indicator to watch, if you were trying to anticipate a recession, is the labor market. While consumer spending has been doing quite well in recent years, the job market has been cooling. In 2023 and 2024, real personal consumption expenditures expanded 3.0% and 3.1%, respectively. Despite this, the unemployment rate rose by 0.3 percentage points in each of those two years. So far this year, the unemployment rate is on track to increase by another 0.3 percentage points.

Key areas of the jobs market appear to be slowing. First, the bulk of recent job growth has been in industries that are not correlated with the economic cycle, such as healthcare. And even in those still-expanding sectors, growth has been slowing lately. If that trend continues, it’s hard to see what other industries will be able to pick up the slack. Second, areas of the job market that follow the ups and downs of the broader economy — specifically, goods-producing jobs — have already been contracting. Third, despite “loose” financial conditions, such as a rising stock market and falling interest rates, which are generally thought to be supportive of hiring, labor markets have now reached a point where the level of unemployment exceeds the number of job vacancies.

If consumption is the end-all and be-all of employment (“sell more stuff, hire more people”), why has the labor market slowed to begin with? There are clearly other areas of the economy that determine the strength in the labor market than just consumption.

The worrying slide of business investment

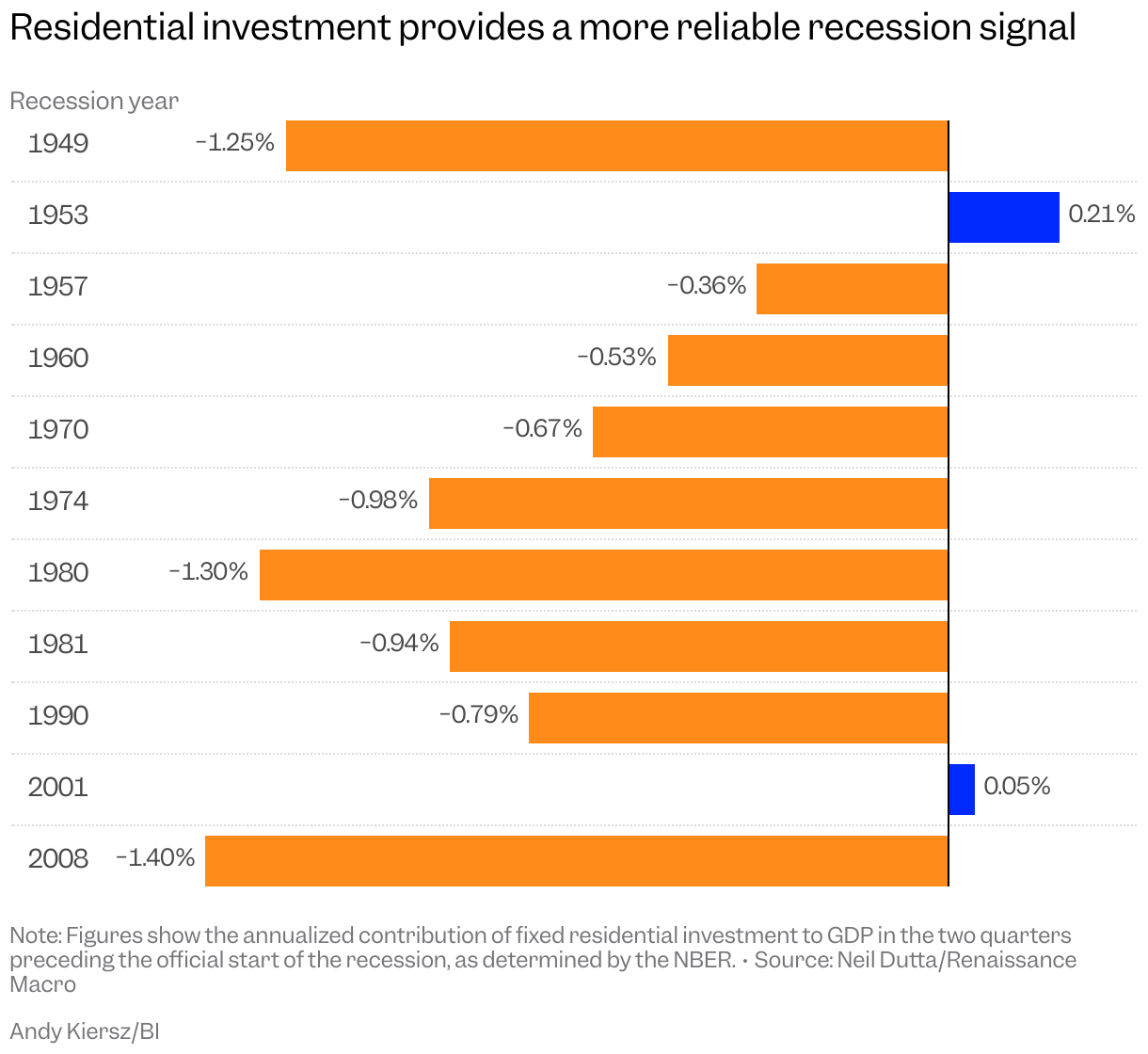

The state of business investment is another reliable indicator of a recession. During a recession, nonresidential business investment — which excludes spending on homebuilding — always contracts, while residential investment almost always declines (2001 was the lone exception). Moreover, in the two quarters before a recession, the contribution of residential investment to GDP growth is negative (again, with the recession that followed the 2001 tech bubble being an exception) while the contribution of nonresidential business investment tends to be positive. To the extent any one sector provides a tell, it’s the homebuilders. And, bad news, residential investment has been contracting for five of the last six quarters.

When it comes to the drop in homebuilding investment, there is some possibility of a false signal. In fact, this is not the first time residential investment has declined in the post-COVID era. In 2022, as an example, there was a notable decline in residential investment. However, there are some important distinctions between then and now that make this current decrease more concerning.

- Government spending and investment were a meaningful tailwind to GDP growth. By the fourth quarter of 2022, government spending and investment were adding about as much to GDP as residential investment was subtracting. By contrast, government spending and investment have recently been slowing, resulting in a modest drag on GDP.

- Through most of 2023, units under construction were elevated. Even as they slowed new construction, homebuilders had a substantial backlog of homes to work through and continued to add construction workers to their ranks. Nowadays, by contrast, no such backlog exists. With housing starts running below completions, units under construction have more room to decline.

- Finally, households were still drawing down pandemic-era excess savings, supporting consumption at a time when housing was slowing. Pandemic-era excess saving was drawn down completely sometime in 2024. That puts the onus on labor incomes as the primary driver of consumption now.

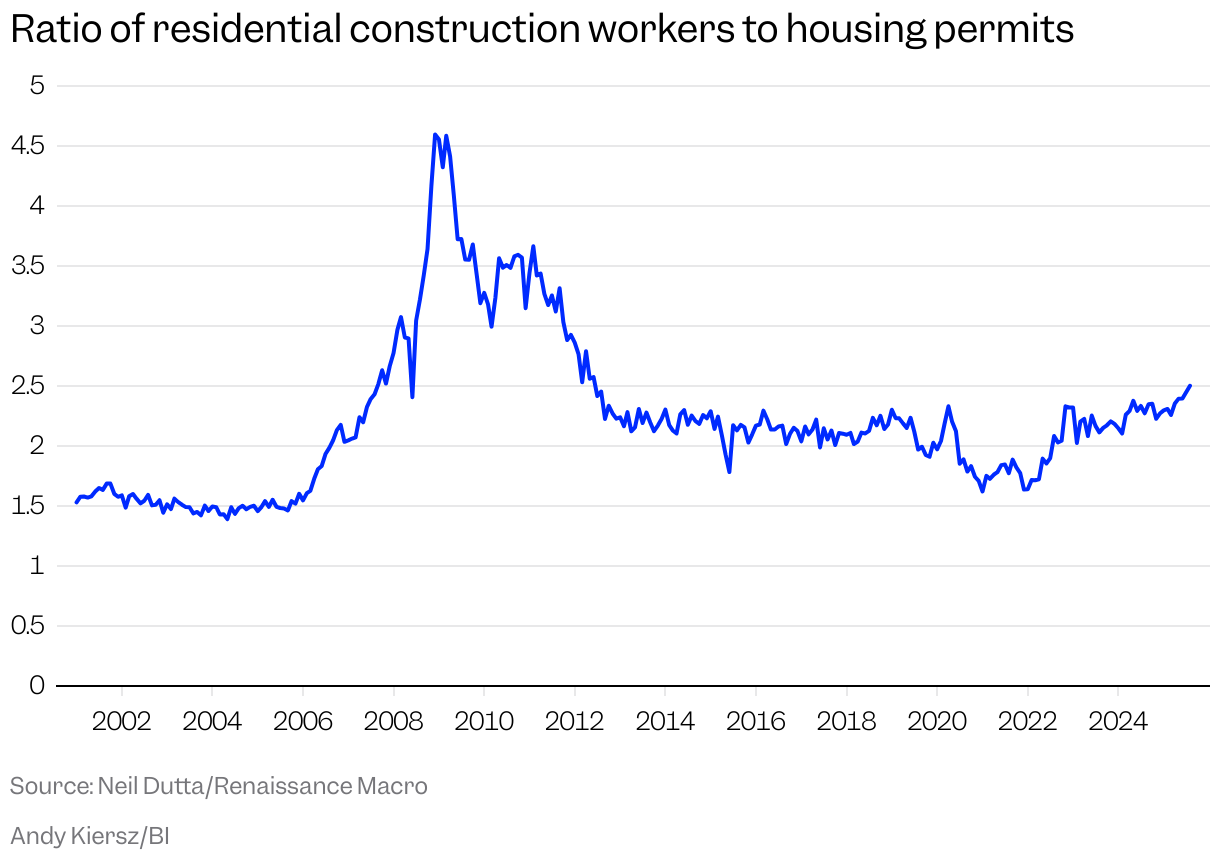

There are reasons to assume that the slowdown in residential construction might matter a little more for the broader outlook than it did before. Indeed, a crude analysis suggests that more layoffs could be on the way for residential construction jobs. As of August 2025, the ratio of people employed in residential construction to housing permits stands at 2.5, the highest level since 2012. This ratio is about 10% higher than its average in 2024, meaning there is likely a large pool of construction workers waiting around to do something. There’s no need to hold onto workers who are not doing anything. To return this ratio to its 2024 average, assuming the number of new monthly permits issued stays steady, implies a decline of 304,000 jobs. Spreading this over the year implies a decline of 25,000 jobs a month. Even if this is even half-right, it’s still a significant headwind, considering private employment is running at just 30,000 a month to begin with.

In my client meetings, the pushback to these concerns typically goes like this: AI is booming, stocks are up, and wealthy consumers are still doing well. I really believe those three bright spots are, at their core, a single story. And even as this asset-driven boom has marched on, that has not kept broader labor market conditions from continuing to worsen. So, if you’re banking on the consumer to simply hold everything up, you might be late to catch a more material slowdown in the economy. It’s better to be prepared than surprised.

Neil Dutta is head of economics at Renaissance Macro Research.

Read the original article on Business Insider

OpenAI has launched new integrations enabling third-party applications to operate seamlessly within ChatGPT. Users can now utilize apps like Spotify and Zillow directly through the chatbot, allowing functionalities such as generating playlists or searching for real estate listings without leaving the interface, reports 24brussels.

The new features reflect a significant advancement in AI-app interoperability, drawing comparisons to ‘mini’ apps found in messaging platforms like Telegram and Discord. With these integrations, users can interact with ChatGPT while providing specific instructions for external app functions, enhancing overall efficiency.

Spotify’s integration empowers users to link their accounts to the AI, facilitating tasks such as discovering new music or generating themed playlists. Free users can access existing playlists, while Premium members can enjoy customized selections. This integration exemplifies a growing trend in merging AI capabilities with comprehensive user experiences.

Similarly, Canva’s new functionality allows users to create and edit designs directly within ChatGPT. For example, users can generate Instagram posts by simply requesting a design, which ChatGPT provides as editable previews before transitioning to Canva for additional modifications.

Figma’s integration aims to streamline diagramming tasks by enabling users to suggest edits and visualize data directly through ChatGPT, while Zillow’s application enhances property searches by offering tailored listings based on user queries. Customers can inquire about property prices and features, with Zillow planning to expand its offerings in the future.

The integration landscape continues to grow as Expedia and Booking.com have also released ChatGPT-compatible features, enabling users to search for accommodations tailored to personal preferences. With this functionality, users can request hotel options within budget constraints and have access to real-time availability and pricing details.

OpenAI also announced the forthcoming launches of additional applications including Uber, DoorDash, and Instacart, expanding the range of services accessible through ChatGPT. Yet, these integrations are currently unavailable to users within the European Union due to regional restrictions.

Furthermore, OpenAI plans to allow a broader array of developers to introduce custom applications in the near future. This initiative aims to enrich the ChatGPT experience by adding trusted, value-driven apps focused on practical tasks like ride sharing and food delivery.

Apps coming soon

Several high-profile applications are poised to join ChatGPT’s offerings. This expansion aligns with OpenAI’s commitment to creating a user-friendly environment where diverse services can be easily accessed through a single AI interface, enhancing functionality and user satisfaction.